Critical Shifts:

-

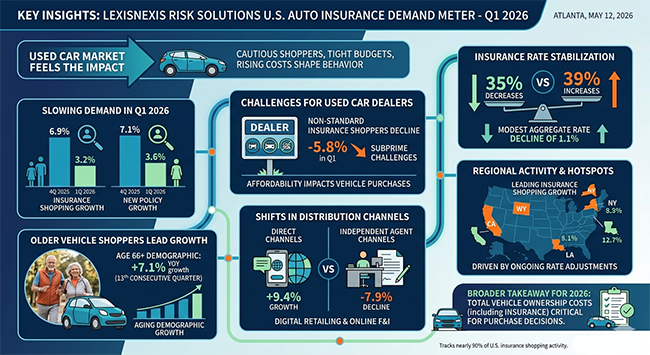

Slowing Insurance Demand: Auto insurance shopping growth slowed significantly in Q1 2026, dropping to 3.2% from 6.9% in the previous quarter, signaling a cooling automotive market and more cautious consumer spending.

-

Affordability Pressures: The "non-standard" insurance segment—typically tied to subprime or high-risk used car buyers—saw a 5.8% decline, highlighting that lower-income households are facing tighter budget constraints.

-

Insurance Rate Stabilization: For the first time in several cycles, the market saw a modest aggregate rate decline of 1.1%, with 35% of insurers rolling out rate decreases as the industry begins to stabilize.

-

Demographic Shift: Older consumers (aged 66+) remain the most active shoppers, leading growth for the 13th consecutive quarter, suggesting a strategic opportunity for dealerships to target this demographic.

-

Channel Migration: There is a sharp divide in how consumers shop; direct insurance channels grew by 9.4%, while independent agent channels plummeted by 7.9%, reflecting a shift toward digital-first shopping experiences.

______________________________________________

As car shoppers grow more cautious in 2026, the used car market is starting to feel the impact. The latest LexisNexis Risk Solutions U.S. Insurance Demand Meter shows auto insurance shopping activity slowing in Q1, another sign that rising ownership costs and tighter household budgets are shaping consumer behavior across the automotive market.

According to the report, year-over-year auto insurance shopping growth slowed to 3.2% in Q1 2026, down from 6.9% in Q4 2025. New policy growth also dropped to 3.6%, compared to 7.1% in the previous quarter. Analysts say the slowdown reflects softer vehicle sales activity and fewer consumers rushing to buy vehicles ahead of anticipated tariff-related price increases seen earlier in 2025.

For independent and used car dealerships, the findings reinforce ongoing affordability challenges impacting both vehicle purchases and ownership costs. LexisNexis Risk Solutions noted that non-standard insurance shoppers — a segment often associated with subprime and higher-risk vehicle buyers common in the used car market — declined 5.8% in Q1 after posting strong growth in late 2025.

The report also highlights how insurance costs continue influencing buying decisions across the used vehicle market. While insurance rate increases previously pushed consumers to aggressively shop for better coverage, Q1 saw more insurers rolling out rate decreases. Overall, 35% of rate revisions were decreases, while 39% were increases, resulting in a modest aggregate rate decline of 1.1%.

For dealerships, especially those operating in the independent and buy-here-pay-here segments, insurance affordability remains a critical factor affecting loan approvals, monthly payment calculations, and overall vehicle affordability.

Another key takeaway for used car retailers is the continued growth among older vehicle shoppers. Consumers aged 66 and older led all demographics in insurance shopping growth for the 13th consecutive quarter, rising 7.1% year over year. The trend suggests dealerships may benefit from marketing more heavily toward older buyers seeking affordable transportation alternatives and lower ownership costs.

The report also revealed major shifts across insurance distribution channels. Direct insurance channels posted the strongest growth at 9.4%, while independent agent channels declined sharply by 7.9%. This transition could further accelerate the use of digital retailing tools and online F&I integration within used dealerships as buyers increasingly seek streamlined purchasing and insurance-shopping experiences.

State-level data showed New York, California, Wyoming, and Louisiana leading the nation in insurance shopping growth. Analysts attributed much of the activity to ongoing insurance rate adjustments in those markets, particularly in states where rate approvals move more slowly.

LexisNexis Risk Solutions executives said customer retention and loyalty will become increasingly important as the insurance market stabilizes after several years of elevated shopping activity.

For independent car dealerships, the broader takeaway is clear: consumers remain highly payment-sensitive, and total vehicle ownership costs — including insurance — continue playing a larger role in vehicle purchase decisions heading into the second half of 2026.

The LexisNexis Risk Solutions U.S. Insurance Demand Meter tracks nearly 90% of U.S. insurance shopping activity and provides quarterly insights into consumer shopping trends, policy growth, and retention behavior across the automotive and insurance industries.