Insights from the 2025 NADA Full-Year Report point to a clear shift: pre-owned vehicles are now the primary driver of independent dealership profitability. As the market moves deeper into 2026, success will depend on disciplined inventory management and smarter wholesale acquisition strategies.

The Used-Vehicle Department: Your Revenue Engine

The used-vehicle department has become the financial core of the modern dealership, accounting for 31.8% of total sales. It’s no longer supporting new car sales—it’s driving cash flow.

The used-vehicle department has become the financial core of the modern dealership, accounting for 31.8% of total sales. It’s no longer supporting new car sales—it’s driving cash flow.

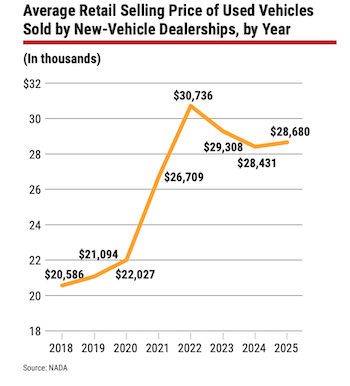

- Average retail price: $28,680 per unit

- Sales productivity: Top performers average 139 units per year

- Revenue growth: Franchised dealers are seeing a 4.5% year-over-year increase, driven largely by higher-margin pre-owned sales

The Credit Landscape: Growth with Caution

Recent data from Cox Automotive and Dealertrack shows a broad expansion in credit availability, helping dealers increase unit volume. However, this comes with rising risk that requires careful oversight.

- Subprime growth: Lending has reached its highest share since 2020, expanding access to more buyers

- Lender activity: Banks are posting strong gains, while captive finance arms are at their most aggressive levels since early 2022

Expanding credit is boosting approvals—but it’s also increasing long-term portfolio risk.

Rising Risk: Defaults and Negative Equity

Rising Risk: Defaults and Negative Equity

The risk side of the equation is becoming harder to ignore:

- Delinquencies: Slightly down to 1.97%

- Defaults: Up to 3.79%—the highest level since 2010

- Year-to-date trend: Defaults are running 9% higher than last year

At the same time, negative equity continues to climb. For the third consecutive month, it has reached record highs. Fewer consumers hold active auto loans, but total balances are increasing—widening the trade-in gap and making it more difficult for buyers to move into new vehicles.

Financing Strategy: The 72+ Month Reality

The average monthly payment for a used vehicle has risen to $537, pushing more buyers into longer loan terms to maintain affordability.

- Nearly 30% of buyers are choosing 73–84 month terms

While extended terms help close deals today, they also delay future trade cycles—reducing near-term repeat business and tightening future inventory pipelines.

Regional Dynamics: Where Growth Is Concentrated

Regional Dynamics: Where Growth Is Concentrated

Geography is becoming a major performance lever, not just a background factor.

- Revenue leaders: Florida leads with average dealership revenue of $129.5 million, followed by California and Nevada

- Volume concentration: California and Texas account for 22.5% of all retail registrations

- Efficiency gains: Virginia and Arizona are outperforming traditional Midwestern markets, with average revenues exceeding $100 million

Aligning inventory with high-growth regions can significantly improve turnover and profitability.

Fixed Ops: A Key Margin Driver

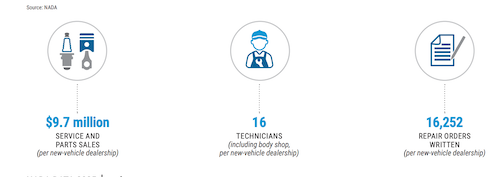

For used-focused dealerships, fixed operations play a critical role in protecting profitability. The average dealership generates $9.7 million annually in service and parts.

In-house reconditioning reduces costs, improves turnaround time, and gives dealers greater control over inventory quality. With internal labor rates averaging $186, dealers can bring vehicles to frontline-ready condition without third-party markups.

The Bottom Line

Through the rest of 2026, the advantage will shift to dealers who prioritize resilience over short-term volume. Expanding credit access will continue to support sales, but rising defaults and persistent negative equity will separate disciplined operators from aggressive ones.

Dealerships should focus on:

- Maintaining a balanced lender mix while tightening deal structure and approval quality

- Prioritizing inventory with strong turn rates over speculative, high-gross units

- Managing aging inventory more aggressively as affordability pressures persist

- Leveraging fixed operations to offset margin compression on the front end

Operations through Q3 and Q4 will reward consistency, cost control, and operational discipline. Dealers who adapt to longer ownership cycles and tighter consumer budgets will be better positioned to protect margins and sustain performance through the end of the year and into 2027.