A proposed 25% tariff on European vehicle imports could gradually reshape pricing, supply, and strategy across the U.S. used car market.

Critical Shifts:

-

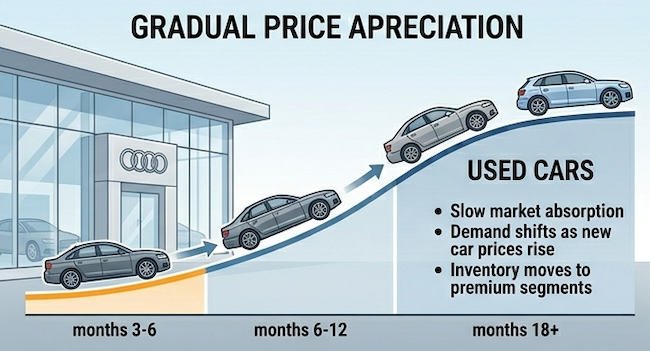

Gradual Value Growth: Used car prices won't spike instantly; instead, they will likely see a steady, long-term rise as expensive new imports drive buyers toward used alternatives.

-

Widening Price Gap: Higher new car prices make late-model used vehicles a more attractive, budget-friendly choice for payment-sensitive consumers.

-

Higher Operating Costs: Tariffs on parts could increase reconditioning and service expenses, potentially squeezing profit margins for independent dealers.

-

Strategic Inventory Selection: Since brands with U.S. factories may be exempt, dealers must focus on specific models rather than assuming all European cars will increase in value.

_________________________________________________

President Trump's latest proposed 25% tariff on European vehicle imports is drawing attention across the automotive industry, but for independent used car dealers, the real question is less about the headline and more about how—and when—this actually changes the market. While the policy is designed to influence manufacturing decisions and trade balances, its practical impact will show up in more familiar territory: pricing dynamics, inventory flow, and operating costs.

The announcement itself was blunt. In a social media post, President Trump tied the move directly to ongoing trade tensions, writing:

“Based on the fact the European Union is not complying with our fully agreed to Trade Deal, next week I will be increasing Tariffs charged to the European Union for Cars and Trucks coming into the United States.”

That position was echoed by U.S. Trade Representative Jamieson Greer, who signaled a broader willingness to recalibrate trade commitments:

“The president decided that if the Europeans aren’t implementing the deal right now, then we don’t have to implement all of it either at this time.”

For dealers, however, the timeline matters more than the rhetoric. Despite the urgency surrounding the announcement, this is not a shift that plays out overnight. The used car market tends to absorb shocks gradually, and the effects of a tariff—especially one filtered through global supply chains and manufacturer strategy—are likely to emerge over quarters, not weeks.

A Gradual Lift, Not an Immediate Surge: There is a logical expectation that higher import costs will support used vehicle values, particularly in the European segment. If new models from brands like BMW and Audi become more expensive, late-model used vehicles naturally become more appealing as substitutes. Over time, that shift in consumer behavior can create upward pressure on used pricing.

But even within the administration’s messaging, there is an acknowledgment that outcomes depend on how manufacturers respond. As Trump noted:

“It is fully understood and agreed that, if they produce Cars and Trucks in U.S.A. Plants, there will be NO TARIFF.”

That distinction matters. Automakers have multiple levers to soften the impact of tariffs, including pricing strategies, dealer incentives, and financing offers. In addition, not all European vehicles are equally exposed. Manufacturers such as Mercedes-Benz and Volkswagen already produce a significant portion of their vehicles in the United States, meaning the tariff’s effect will vary by model and production origin.

While much of the focus is on downstream effects in the used market, the upstream impact on manufacturers is already visible. European auto stocks moved lower following the announcement, with the regional autos and parts index falling roughly 2%, while shares of major manufacturers—including Porsche, BMW, Mercedes-Benz, and Volkswagen—declining between 2% and 3% in early trading.

German automakers, in particular, appear most exposed. Volkswagen Group has already absorbed an estimated $4.7 billion in tariff-related costs in 2025, and analysts warn that additional measures could deepen the impact. According to Bernstein Research, a further escalation could reduce operating profits for German manufacturers by another $3 billion.

There are also early signs of demand softening. U.S. retail sales for Audi and Porsche were already down—by roughly 30% and 12%, respectively—in the first quarter, even before the latest tariff proposal intensified pressure on pricing and consumer sentiment.

For independent dealers, this suggests a more measured outlook. Rather than a sudden spike in inventory value, the more realistic scenario is a gradual strengthening in demand for well-positioned used units, particularly in the near-luxury and premium segments.

The Real Opportunity Lies in the Price Gap: Where the impact becomes more meaningful is in the widening gap between new and used vehicle pricing. Even modest increases in new car costs can shift consumer decision-making, especially among buyers who are already sensitive to monthly payments.

As that gap grows, late-model used vehicles begin to look less like a compromise and more like a rational choice. Independent dealers are well positioned to benefit from this shift, particularly those with access to clean, well-reconditioned inventory that can closely compete with new alternatives in both quality and presentation.

That said, this advantage develops over time. Consumer behavior does not pivot instantly, and the perception of value evolves as pricing differences become more visible in the marketplace.

Inventory Decisions Require Discipline, Not Urgency: One of the more immediate risks for independent dealers is overreacting to the headline itself. While it is tempting to anticipate tighter supply and move aggressively in the wholesale market, current inventory pipelines remain largely unchanged in the short term. Lease returns, trade-ins, and auction volumes are still flowing through established channels.

If tariffs begin to meaningfully reduce import volumes, the effects will likely appear later in the year or early 2027, not within the current buying cycle. In the meantime, auction markets may experience pockets of volatility as some dealers position early, but sustained pricing shifts typically require consistent supply-side pressure.

Production Shifts Are a Long-Term Variable: The broader policy goal—encouraging automakers to expand U.S.-based production—adds another layer of complexity, but not one that will resolve quickly. Speaking to reporters, Trump emphasized the intended pressure on manufacturers:

“So I raised the tariffs on cars and trucks to 25%, that's billions of dollars coming into the United States, and it forces them to move their factory production much faster.”

In practice, however, production shifts operate on a much longer timeline. Even with existing U.S. facilities, scaling production or reallocating supply chains is a multi-year process influenced by cost structures, labor considerations, and regulatory stability.

Ongoing uncertainty surrounding the review of the United States-Mexico-Canada Agreement further complicates those decisions. As a result, any increase in the supply of tariff-exempt vehicles is unlikely to provide meaningful relief in the near term. For dealers, this reinforces the idea that current conditions will persist longer than the initial announcement might suggest.

Rising Costs on the Service Side: While much of the focus remains on vehicle pricing, the more immediate and consistent pressure may come from the cost side of the business. If tariffs extend to automotive components—or if broader trade tensions disrupt parts supply chains—dealers could see incremental increases in the cost of reconditioning and service operations.

European vehicles, which already carry higher parts and labor costs, may become more expensive to bring to frontline condition. This has a direct impact on profitability, particularly for independent dealers who rely on efficient turnaround and tight cost control. Service departments may also face margin compression if higher input costs cannot be fully passed on to customers.

Unlike vehicle pricing, which fluctuates with market demand, these cost increases tend to be more persistent and harder to offset.

Consumer Behavior Remains the Deciding Factor: Ultimately, the extent to which dealers benefit from these changes depends on the consumer. Higher new vehicle prices can push buyers toward the used market, but affordability remains a limiting factor. With financing costs still elevated, many buyers are already operating within constrained budgets.

This creates a more balanced outlook. Demand for used vehicles may strengthen, particularly in segments directly affected by import pricing, but there are limits to how much additional cost the market can absorb. Dealers who assume unrestricted pricing power risk misreading the customer.

A Market Shift—But on Real-World Timelines: The proposed 25% tariff has the potential to influence the used car market in meaningful ways, particularly by reinforcing the value proposition of late-model used inventory. However, the transition will be gradual, uneven, and shaped by multiple variables beyond the policy itself.

For independent dealers, this is less a moment of immediate opportunity and more a period that rewards careful positioning. Monitoring wholesale trends, managing acquisition costs, and maintaining flexibility in inventory strategy will matter more than reacting to early speculation.